Is MSTR a Leveraged Bitcoin Proxy? Rolling Beta Analysis in Python

June 5, 2026

What's the question?

MicroStrategy, now trading as MSTR, is often treated as an equity wrapper for Bitcoin exposure. That framing is useful, but incomplete. An equity can move with Bitcoin and still carry additional risk from leverage, operating-company structure, financing, index flows, and investor positioning.

The practical question is whether MSTR behaves like a one-for-one Bitcoin proxy or like a leveraged exposure. Beta answers that question. Beta measures the sensitivity of one return series to another. A beta of 1.50 to IBIT means that, historically, MSTR moved about 1.5% for every 1.0% move in IBIT, before considering company-specific noise.

This matters for position sizing. If a portfolio manager treats MSTR as ordinary equity exposure, the portfolio may contain more Bitcoin-linked risk than intended.

The approach

The test compares MSTR with IBIT, COIN, MARA, and RIOT from January 11, 2024, the start of IBIT trading history in the data. Built from SEC EDGAR public filings and market data, the analysis uses daily split-adjusted prices.

- Pull daily prices for the Bitcoin-linked basket

- Calculate daily returns from

adj_close - Estimate full-sample beta and correlation to IBIT

- Calculate rolling 60-day beta and correlation for MSTR

- Compare annualized volatility and max drawdown across the basket

The benchmark is IBIT because it is the cleanest listed Bitcoin-linked reference in the sample. COIN, MARA, and RIOT provide an equity peer group.

Code

import xfinlink as xfl

import pandas as pd

xfl.set_api_key("YOUR_API_KEY") # free at https://xfinlink.com/signup

tickers = ["MSTR", "IBIT", "COIN", "MARA", "RIOT"]

df = xfl.prices(tickers, start="2024-01-11", fields=["adj_close"])

prices = df.pivot_table(index="date", columns="ticker", values="adj_close")[tickers].dropna()

returns = prices.pct_change(fill_method=None).dropna()

stats = []

for ticker in tickers:

beta = returns[ticker].cov(returns["IBIT"]) / returns["IBIT"].var()

corr = returns[ticker].corr(returns["IBIT"])

vol = returns[ticker].std() * (252 ** 0.5)

drawdown = (prices[ticker] / prices[ticker].cummax() - 1).min()

stats.append([ticker, beta, corr, vol, drawdown])

print(pd.DataFrame(stats, columns=["ticker", "beta", "corr", "vol", "max_drawdown"]))Full script with formatting and visualisation: mstr-bitcoin-proxy-beta-python.py

Output

=== MSTR Bitcoin-Proxy Beta Test ===

Sample: 2024-01-12 to 2026-06-04 (599 trading days)

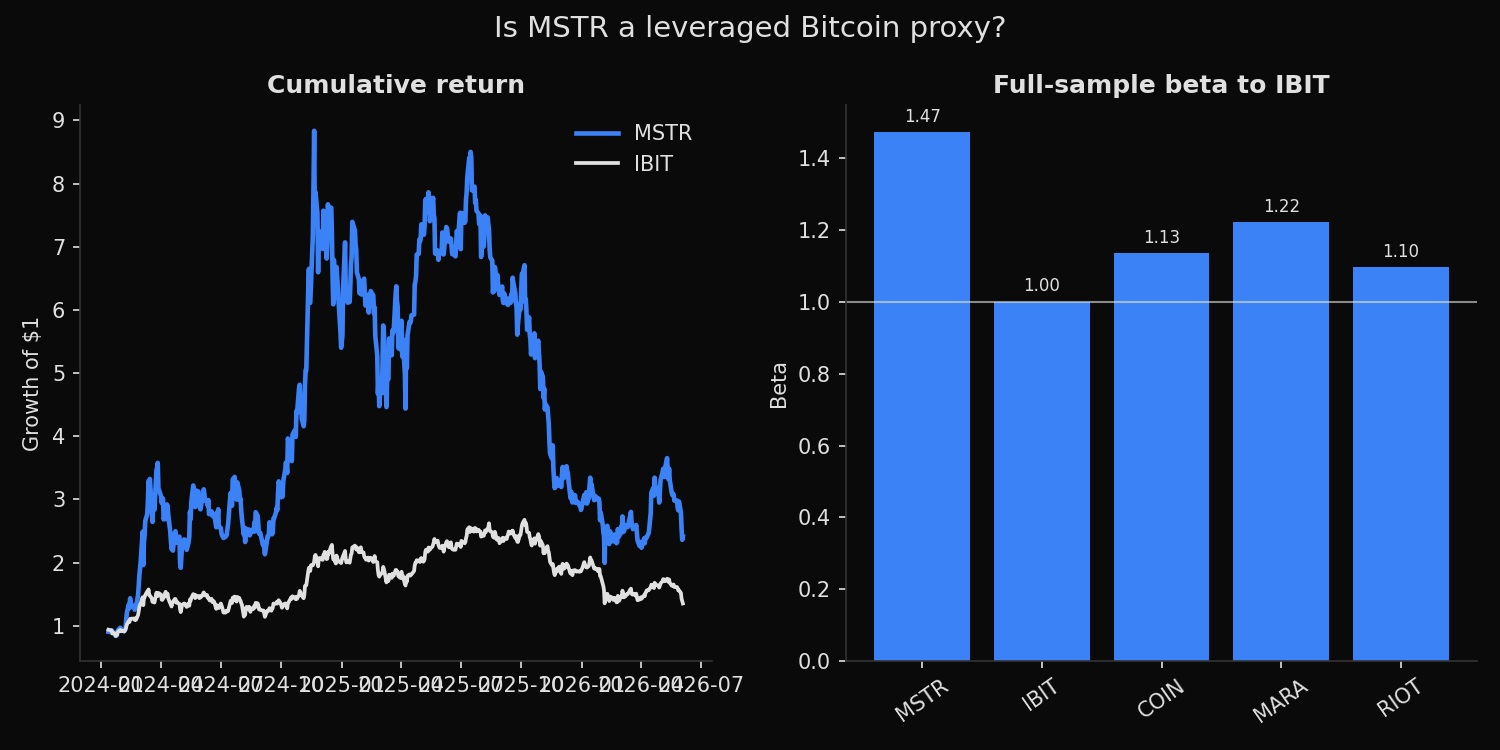

MSTR full-sample beta to IBIT: 1.47

MSTR latest 60-day beta to IBIT: 1.66

MSTR full-sample correlation: 0.79

MSTR latest 60-day correlation: 0.84

MSTR annualized volatility: 93.3%

IBIT annualized volatility: 50.3%

MSTR max drawdown: -77.4%

IBIT max drawdown: -49.5%

MSTR up-capture on IBIT +3% days: 1.52x

MSTR down-capture on IBIT -3% days: 1.34x

Bitcoin-linked equity ranking:

MSTR beta= 1.47 corr=0.79 vol= 93.3% max_drawdown= -77.4%

MARA beta= 1.22 corr=0.66 vol= 92.4% max_drawdown= -78.3%

COIN beta= 1.13 corr=0.72 vol= 79.5% max_drawdown= -66.4%

RIOT beta= 1.10 corr=0.62 vol= 89.0% max_drawdown= -64.3%

IBIT beta= 1.00 corr=1.00 vol= 50.3% max_drawdown= -49.5%What this tells us

MSTR behaves like a leveraged Bitcoin-linked equity, not a one-for-one Bitcoin proxy. Its full-sample beta to IBIT is 1.47, and the latest 60-day beta is higher at 1.66. Correlation is also high. The full-sample correlation is 0.79, while the latest 60-day correlation is 0.84.

The risk difference is visible in volatility and drawdown. MSTR annualized volatility is 93.3%, compared with 50.3% for IBIT. MSTR max drawdown is -77.4%, compared with -49.5% for IBIT. The down-capture ratio is 1.34x on days when IBIT falls at least 3%, which means MSTR has historically amplified large downside Bitcoin moves.

MSTR also has the highest beta in the peer group. MARA, COIN, and RIOT all have positive Bitcoin sensitivity, but none exceed MSTR on this measure.

So what?

MSTR should be sized as leveraged Bitcoin-linked exposure. A 5% position in MSTR is not economically similar to a 5% position in IBIT. Based on this sample, its beta-adjusted Bitcoin exposure is closer to 7% to 8%, and the drawdown profile is materially worse.

For portfolio construction, the useful control is not the ticker label. It is the estimated beta and down-capture ratio. If those measures keep rising, MSTR becomes less useful as a diversified equity holding and more useful only as an explicit high-conviction Bitcoin risk position.

Built with xfinlink — free financial data API for Python. pip install xfinlink

pip install xfinlink