Do Low-Volatility S&P 500 Stocks Reduce Drawdowns? Factor Test in Python

June 5, 2026

What's the question?

Low-volatility investing is based on a simple claim: stocks with lower realized volatility should produce smoother portfolio outcomes. The claim is not that low-volatility stocks always outperform. The claim is that they can reduce drawdowns and improve risk control.

That distinction matters. In a strong risk-on market, high-volatility stocks may produce higher returns. A low-volatility factor can still be useful if it limits downside when conditions deteriorate. The practical question is whether low-volatility S&P 500 members reduced drawdowns over the last year, using the index membership that existed at the start of the test.

Using point-in-time membership matters because it avoids looking only at today's surviving index members.

The approach

The universe starts with S&P 500 constituents as of June 5, 2025. The script then intersects that index membership with a liquid common-stock candidate set and requires current price coverage. Built from SEC EDGAR public filings and market data, the analysis uses daily split-adjusted prices through June 4, 2026.

- Pull S&P 500 membership with

as_of="2025-06-05" - Pull daily prices for the liquid member subset

- Calculate realized annualized volatility for each stock

- Build the 10 lowest-volatility and 10 highest-volatility baskets

- Compare average total return and max drawdown

The result is a factor diagnostic, not a complete portfolio backtest.

Code

import xfinlink as xfl

import pandas as pd

xfl.set_api_key("YOUR_API_KEY") # free at https://xfinlink.com/signup

members = xfl.index("sp500", as_of="2025-06-05", limit=500)

tickers = sorted(set(members["ticker"]))[:100]

df = xfl.prices(tickers, start="2025-06-05", fields=["adj_close"])

prices = df.pivot_table(index="date", columns="ticker", values="adj_close").dropna(axis=1, thresh=200)

returns = prices.pct_change(fill_method=None).dropna()

vol = returns.std() * (252 ** 0.5)

low_vol = vol.nsmallest(10).index

high_vol = vol.nlargest(10).index

print("Low-vol basket return", (prices[low_vol].iloc[-1] / prices[low_vol].iloc[0] - 1).mean())

print("High-vol basket return", (prices[high_vol].iloc[-1] / prices[high_vol].iloc[0] - 1).mean())Full script with formatting and visualisation: sp500-low-volatility-drawdown-python.py

Output

=== Point-in-Time S&P 500 Low-Volatility Drawdown Test ===

Constituent date: 2025-06-05

Price sample: 2025-06-06 to 2026-06-04 (249 trading days)

Tested liquid member subset: 53 stocks

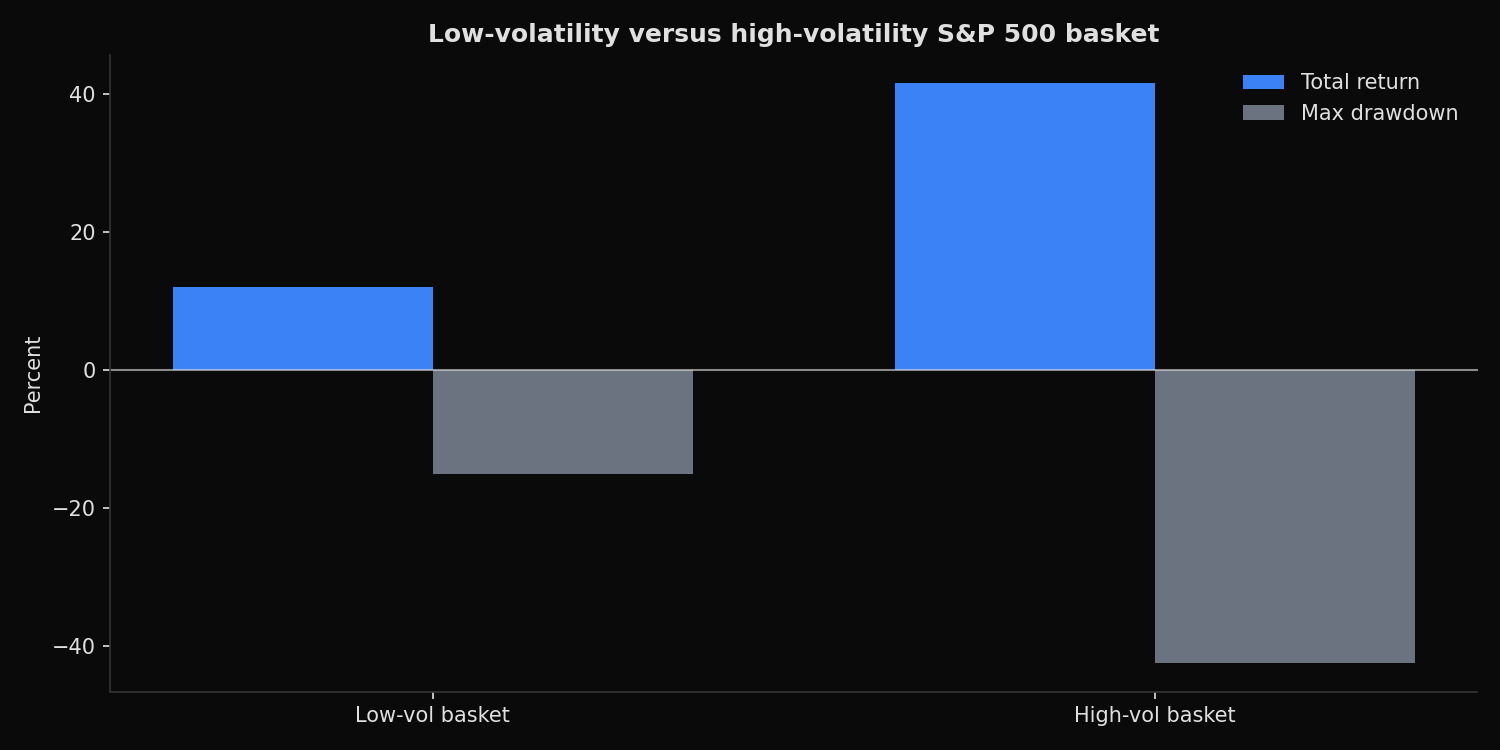

Basket comparison:

Low-vol basket volatility= 19.0% total_return= 12.0% max_drawdown= -15.1%

High-vol basket volatility= 46.8% total_return= 41.5% max_drawdown= -42.5%

Lowest-volatility stocks:

KO vol= 16.2% return= 8.3% max_drawdown= -9.2%

MCD vol= 16.4% return= -11.7% max_drawdown= -20.0%

JNJ vol= 16.8% return= 48.5% max_drawdown= -11.0%

LIN vol= 16.9% return= 7.9% max_drawdown= -19.5%

PG vol= 18.1% return= -13.5% max_drawdown= -16.2%

COST vol= 18.8% return= -3.8% max_drawdown= -16.3%

UNP vol= 21.3% return= 19.6% max_drawdown= -12.3%

JPM vol= 21.7% return= 18.7% max_drawdown= -15.5%

PEP vol= 21.8% return= 8.4% max_drawdown= -17.0%

CVX vol= 22.2% return= 37.6% max_drawdown= -14.0%What this tells us

The low-volatility basket did reduce drawdown. Its average max drawdown is -15.1%, compared with -42.5% for the high-volatility basket. Realized volatility also separates cleanly: 19.0% for the low-volatility group versus 46.8% for the high-volatility group.

The tradeoff is return. The low-volatility basket returned 12.0%, while the high-volatility basket returned 41.5%. In this sample, riskier stocks were rewarded, but they required much larger drawdown tolerance.

The individual low-volatility list is intuitive. KO, MCD, JNJ, LIN, PG, COST, UNP, JPM, PEP, and CVX include staples, healthcare, industrial, financial, and energy exposure. The factor is not sector-neutral. It naturally tilts away from the most speculative growth names.

So what?

Low volatility is a drawdown-control tool, not a guaranteed return enhancer. It can be valuable when the portfolio objective is smoother compounding, lower risk-budget use, or better behavior in selloffs. It can lag when market leadership rewards high-beta exposure.

For portfolio construction, the factor should be judged against its job. If the mandate is absolute return in a risk-on year, low volatility may disappoint. If the mandate is to keep drawdowns within a defined limit, the low-volatility basket did what it was supposed to do.

Built with xfinlink — free financial data API for Python. pip install xfinlink

pip install xfinlink