Is Micron's Memory Cycle Recovering? Inventory and Margin Forecasting in Python

June 5, 2026

What's the question?

Micron is one of the clearest public-market ways to study the memory semiconductor cycle. Memory markets are cyclical because supply is capital intensive and demand can change quickly. When the cycle improves, revenue often rebounds first. Margins and free cash flow usually matter more because they show whether the rebound is becoming economically durable.

The question is whether Micron's latest annual results show a high-quality recovery or only a revenue rebound. A high-quality recovery should combine revenue growth, rising margins, controlled inventory, and positive free cash flow. Inventory matters because excess inventory can signal that demand is being pulled forward or that pricing power remains weak.

The approach

The peer set is MU, NVDA, AMD, INTC, AVGO, and QCOM. The group covers memory, accelerated computing, CPUs, connectivity, and diversified semiconductor exposure. Built from SEC EDGAR public filings and market data, the analysis uses the latest two annual observations for each company.

- Pull revenue, gross profit, operating income, inventory, free cash flow, and capital expenditure

- Calculate revenue growth, gross margin, operating margin, inventory as a share of revenue, inventory growth, and free-cash-flow margin

- Build a cycle score from standardized revenue growth, gross margin, free-cash-flow margin, and inventory intensity

- Rank Micron against the peer set

The score is not a valuation model. It is a compact way to separate a real operating recovery from a lower-quality rebound.

Code

import xfinlink as xfl

import pandas as pd

xfl.set_api_key("YOUR_API_KEY") # free at https://xfinlink.com/signup

tickers = ["MU", "NVDA", "AMD", "INTC", "AVGO", "QCOM"]

fields = ["revenue", "gross_profit", "operating_income", "inventory", "free_cash_flow"]

df = xfl.fundamentals(tickers, period_type="annual", period="6y", fields=fields)

recent = df.sort_values(["ticker", "period_end"]).groupby("ticker").tail(2)

latest = recent.groupby("ticker").tail(1).set_index("ticker")

prior = recent.groupby("ticker").head(1).set_index("ticker")

screen = pd.DataFrame(index=latest.index)

screen["revenue_growth"] = latest["revenue"] / prior["revenue"] - 1

screen["gross_margin"] = latest["gross_profit"] / latest["revenue"]

screen["inventory_to_revenue"] = latest["inventory"] / latest["revenue"]

screen["free_cash_flow_margin"] = latest["free_cash_flow"] / latest["revenue"]

print(screen.sort_values("free_cash_flow_margin", ascending=False))Full script with formatting and visualisation: micron-memory-cycle-forecast-python.py

Output

=== Micron Memory-Cycle Forecast Screen ===

Latest annual periods: 2025-08-28 to 2026-01-25

MU revenue growth: 48.9%

MU gross margin: 39.8%

MU operating margin: 26.1%

MU inventory / revenue: 22.4%

MU inventory growth: -5.9%

MU free-cash-flow margin: 4.5%

MU cycle score rank: 5 of 6

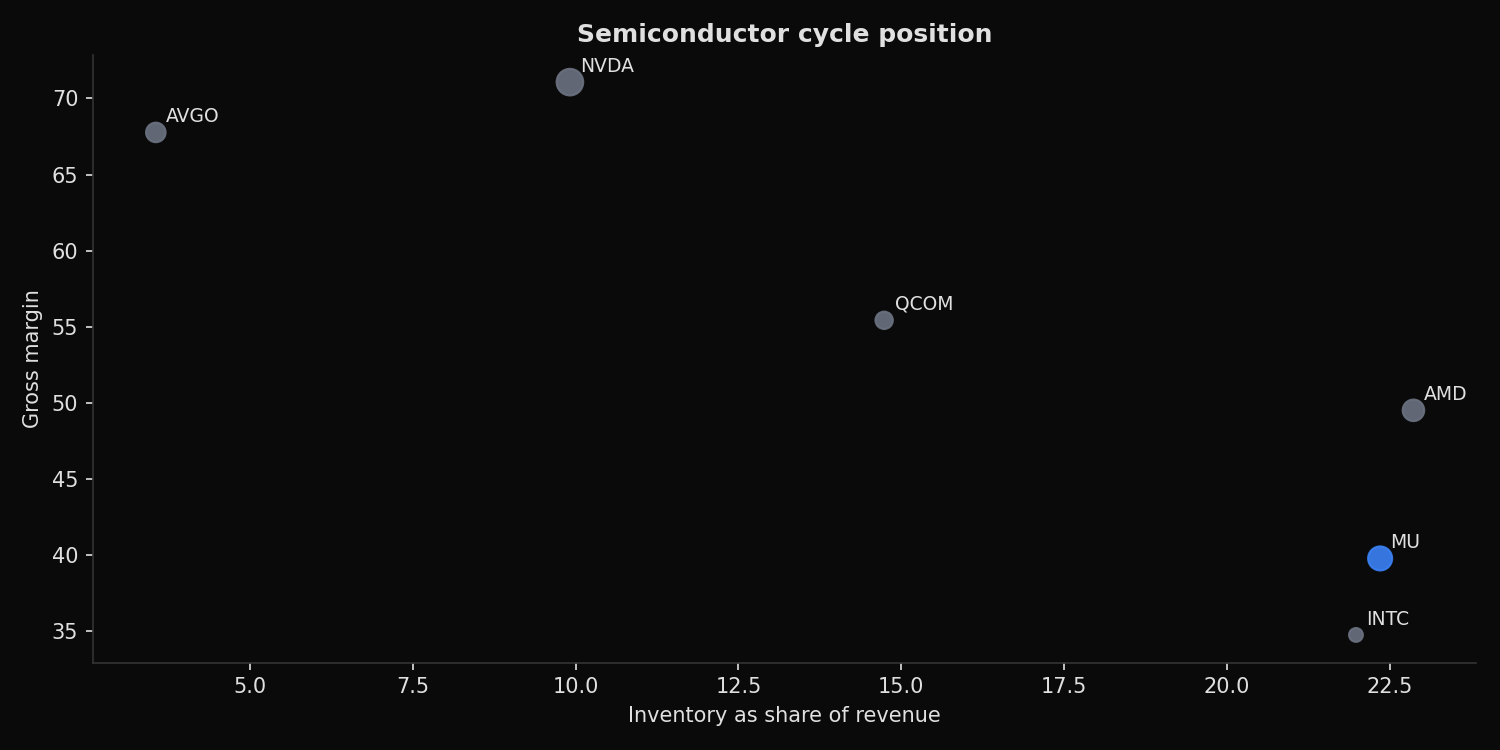

Semiconductor cycle ranking:

NVDA score= 4.94 revenue_growth= 65.5% gross_margin= 71.1% inventory/revenue= 9.9% FCF_margin= 44.8%

AVGO score= 3.53 revenue_growth= 23.9% gross_margin= 67.8% inventory/revenue= 3.6% FCF_margin= 42.1%

QCOM score= -0.08 revenue_growth= 13.7% gross_margin= 55.4% inventory/revenue= 14.7% FCF_margin= 28.9%

AMD score= -1.19 revenue_growth= 34.3% gross_margin= 49.5% inventory/revenue= 22.9% FCF_margin= 19.4%

MU score= -1.95 revenue_growth= 48.9% gross_margin= 39.8% inventory/revenue= 22.4% FCF_margin= 4.5%

INTC score= -5.25 revenue_growth= -0.5% gross_margin= 34.8% inventory/revenue= 22.0% FCF_margin= -9.4%What this tells us

Micron's revenue recovery is real. Revenue growth is 48.9%, and inventory fell 5.9%. That combination is consistent with a memory-cycle rebound because demand is improving while inventory is not rising.

The quality of the rebound is weaker than the revenue number suggests. MU gross margin is 39.8%, operating margin is 26.1%, and free-cash-flow margin is only 4.5%. The cycle score ranks MU fifth of six, ahead of INTC but behind NVDA, AVGO, QCOM, and AMD.

The peer comparison explains the rank. NVDA and AVGO combine high margins with much lower inventory intensity. QCOM has slower growth but stronger free-cash-flow conversion. AMD has similar inventory intensity but a higher free-cash-flow margin. Micron is improving, but it has not yet converted the rebound into peer-leading cash economics.

So what?

Micron can be a cyclical recovery trade without being a high-quality compounding trade. The useful monitor is whether free-cash-flow margin follows revenue growth higher. If MU revenue keeps rising while inventory stays controlled and free cash flow expands, the recovery broadens. If growth remains strong but free-cash-flow margin stays near 4% to 5%, the trade depends more on cycle timing than on durable profitability.

For investors, the signal is clear: revenue confirms the rebound, but free cash flow confirms the quality of the rebound.

Built with xfinlink — free financial data API for Python. pip install xfinlink

pip install xfinlink